Transportation's Share of U.S. GDP Slips to 6.3% in 2024: What It Means for Freight and Logistics

- Kelsea Ansfield

- Feb 24

- 3 min read

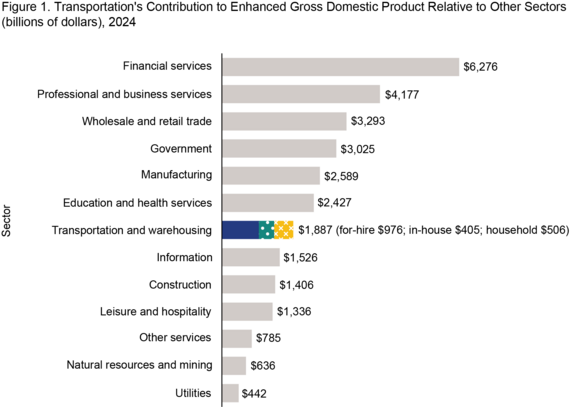

The U.S. Department of Transportation's Bureau of Transportation Statistics (BTS) released its updated Transportation Satellite Accounts (TSAs) today, showing that transportation services contributed $1.9 trillion—or 6.3%—to an enhanced U.S. gross domestic product (GDP) of $29.8 trillion in 2024. While still a substantial economic force, this marks the second consecutive year of decline from a post-pandemic peak of 6.6% in 2022.

The TSAs provide a comprehensive view by capturing three distinct categories of transportation activity:

For-hire transportation — $976 billion (3.3% of enhanced GDP): Commercial services provided by trucking, rail, air, water, transit, parcel delivery, warehousing, and other for-hire modes.

In-house transportation — $405 billion (1.4%): Transportation activities performed by non-transportation businesses for their own operations (e.g., company fleets).

Household transportation — $506 billion (1.7%): Personal motor vehicle use by households.

Including in-house and household contributions nearly doubles the visible economic footprint of transportation compared to standard GDP measures, elevating it from the 10th to the 7th largest contributor among 13 major sectors in 2024.

A Continued Slide from the 2022 High

The drop to 6.3% in 2024 reflects broad-based softening:

For-hire air, rail, and truck transportation combined fell 0.1 percentage points from 2023, returning to its 2021 level of 1.6%.

Household transportation (personal vehicle use) also declined 0.1 percentage points, reverting to 1.7% (2021 level).

In-house transportation held steady at 1.4% from 2021–2024.

All other for-hire modes (transit, parcel/courier, warehousing, sightseeing, etc.) remained flat at 1.6% from 2023 but were down slightly from 2021–2022 peaks.

These trends align with broader post-pandemic normalization: reduced air travel volumes, moderated freight demand growth after the 2021–2022 surge, and shifts in household driving patterns as remote work and fuel prices influenced behavior.

Why This Matters for Freight, Logistics, and Supply Chains

Transportation's declining GDP share doesn't signal industry contraction—total contribution still reached $1.9 trillion—but it highlights evolving dynamics:

Freight intensity — Goods movement (especially trucking and rail) remains vital, but slower growth in for-hire modes suggests shippers are optimizing leaner networks and higher asset utilization.

E-commerce and parcel resilience — Warehousing, courier, and delivery services (part of "all other for-hire") have held steady, reflecting sustained demand for last-mile and fulfillment infrastructure.

Capacity and investment signals — Stable in-house transportation indicates businesses continue relying on private fleets, while for-hire softness may ease pressure on carrier rates in some segments.

Household trends — Lower personal vehicle contribution could reflect fuel costs, urban shifts, or increased use of ride-hailing/transit—potentially influencing urban freight patterns and delivery density.

The data underscores that transportation remains a foundational economic driver, even as its relative share normalizes from pandemic highs.

Strategic Takeaways for Shippers and Carriers

At Gain Consulting LLC, we interpret the TSA data as a call to refine efficiency and adaptability:

Optimize mode mix — With for-hire air/rail/truck softening, explore multimodal and intermodal options to capture cost and capacity advantages.

Focus on last-mile and warehousing — Steady contributions in parcel, courier, and storage highlight ongoing demand—invest in network density and technology here.

Monitor household trends — Shifts in personal vehicle use may reshape urban delivery patterns; plan for denser, more flexible last-mile solutions.

Benchmark performance — Use TSA visualizations to compare your operations against sector-wide trends and identify improvement areas.

The full 2024 Transportation Satellite Accounts—including interactive tools on contribution by mode, industry usage, and sector snapshots—are available on the BTS website.

If these macroeconomic shifts are influencing your freight strategy, capacity planning, or rate negotiations, contact Gain Consulting LLC today. We're here to help translate BTS data into actionable supply chain advantages.

Follow us on X @gainconsulting_ for ongoing insights into transportation economics, freight trends, and logistics optimization.

Comments